Taught for: Bachelor Students in Machine Learning, Math & Finance

Abstract

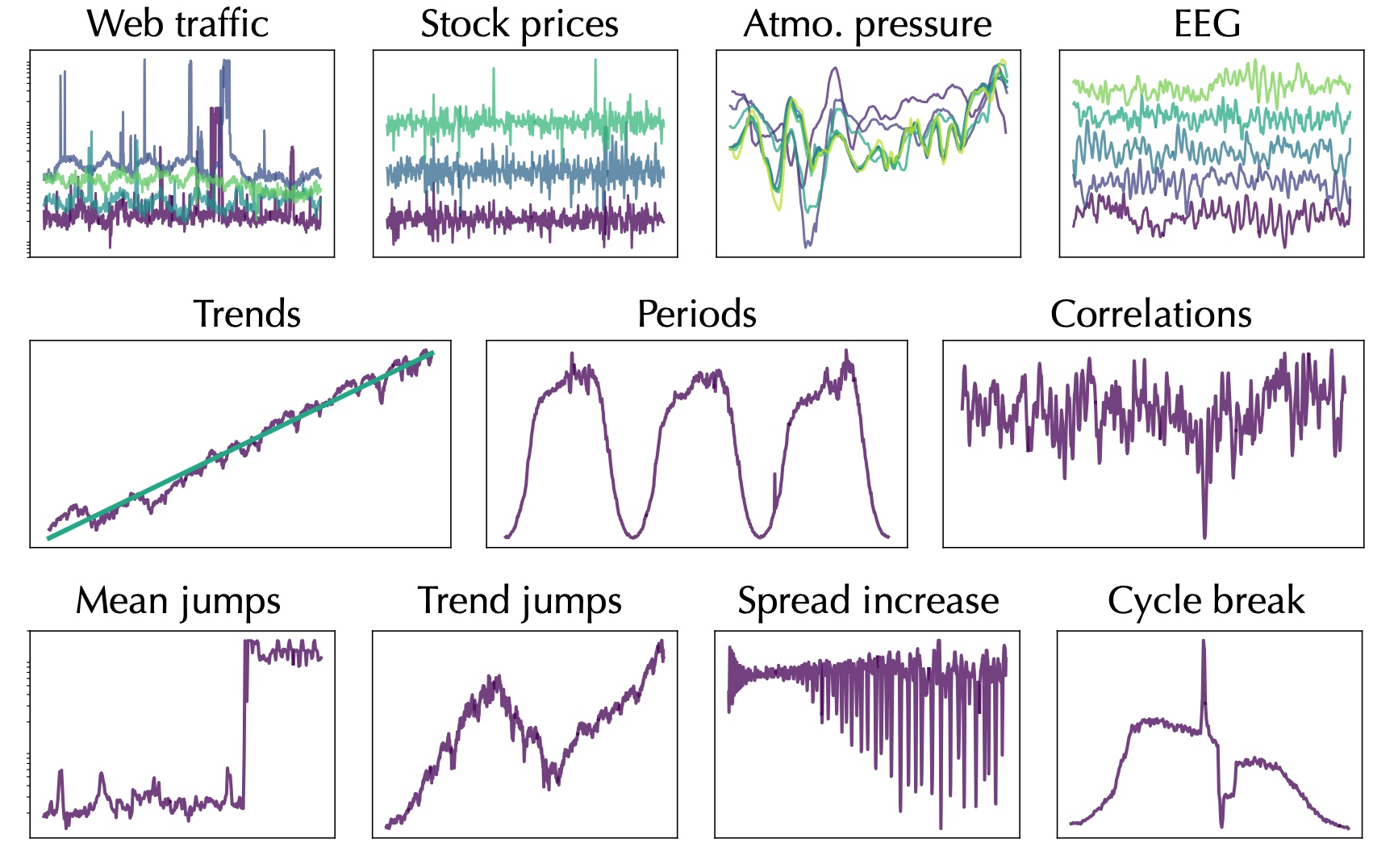

This course provides an introduction into stochastic processes, fundamental to understanding randomness and uncertainty in various systems. We start with the theoretical underpinnings of stochastic processes, including Wiener and Poisson type processes, Markov chains, and Markov processes. Practical aspects such as generating realizations of random processes will also be covered. Advanced topics will include Gaussian and conditional Gaussian models, Hidden Markov Models, and multivariate Gaussian estimation using techniques such as the Kalman filter. The course will also touch upon decision theory, introducing key statistics and tests crucial for making informed decisions in uncertain environments. More practical applications such as anomaly and change-point detection will be considered, demonstrating the relevance of stochastic processes in addressing real-world challenges across various domains.

Course Contents

Lecture 1. Stochastic processes and their characteristics.

Lecture 2. Theory fundamentals of stochastic processes.

Lecture 3. Wiener and Poisson type processes. Generation of realizations of random processes.

Lecture 4. Markov chains.

Lecture 5. Markov processes.

Lecture 6. Stochastic models with discrete time.

Lecture 7. Gaussian and conditional Gaussian models.